ABC cost model to the city of Barcelona

The City Council has decided to develop ABC costing methodology for activity built on the concept of integrated management (total quality, continuous improvement activities, etc.). This system not only allows costs to comply with the law in the presentation of the annual costs and performance of the services required and the calculation of taxes and fees, but that is what can help identify key service, and therefore, improve decision making.

The ABC cost system represents a very important conceptual change regarding traditional systems of costs, allowing to determine the actual cost of a service based on the analysis of the activities developed for their benefit, and the costs are attributable to such activities.

The most remarkable features of the system costs the council are:

- Transverse: allocating different resources used to provide a service independent of the structure of the budget. A service or activity may involve various fields and system cost can impute costs, regardless of who manages the budget. For example, personnel costs.

- Annuity cost: are applied in study costs, apart from the budgetary allocation.

- Map of activities and services: activities are classified into large areas of municipal action (process). Within each process, and tree structure, you can locate the activities and services (mandatory and not mandatory) that makes the City Council.

- Indirect costs: these are costs relating to services but not directly applicable and that makes it require allocation criteria for their allocation to services. In the system of Barcelona some overhead costs are applied according to the ABC system costs (cost drivers) and others following traditional criteria (unit cost). They are, for example, the costs of information technology, municipal structure, office, etc.

The first step in system costs is defined as cost and where they are located. In the case of the City Council, the proposed cost structure independent of the existing budgetary structure, where the main objective is to order costs based on the action areas of the City. The concepts used are:

- PROCESS: Large areas of action of the City Council. Given that all costs must locate, define operational processes and process structure. It is understood by those business processes that include activities and services provided directly to citizens, structure and processes of those not directly related to the provision of services, but they are part of the internal structure of the City it will be passed as indirect costs.

- SUBPROCESS: Example: in the Planning process, some threads are Urban Planning and Action.

- ACTIVITY: the thread is broken down still further. Example: in the thread Urban Action of the activities is processing files and reports.

- TASK: It is broken down activity still further. Example: the activity of processing files and reports, has tasks: building permits and increased activity and discipline records.

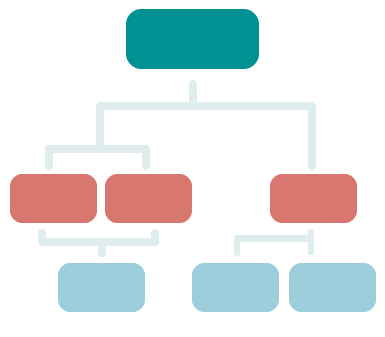

The cost structure is defined so that a process consists of multiple threads, which in turn consist of different activities, which are divided into different tasks. That is, this terminology intends to classify the cost of the service being provided from less to more precision.

The main processes or cost units identified in the costing of the City Council are:

- Urban Development

- Environment

- Urban Infrastructure and Coordination

- Housing

- Quality of life

- Sports

- Mobility

- Police

- Services Prevention and Fire Fighting and Rescue (SPEIS)

- Education

- Culture

- Economic Promotion

- Districts